Market View from Realm Investment Management – week ending 2nd September 2022

Equity Markets were lower last week as investors assessed the implications of the previous week’s hawkish Jackson Hole address by Federal Reserve Chairman Jerome Powell. US Treasury Yields moved higher with the 10Y Treasury yield rallying further from its August low, back towards its June high.

It is looking increasingly unlikely to most commentators that the US economy will be able to avoid a recession altogether, especially as the Fed will not want to ease policy too soon as it did in the 1970s. According to Deutsche Bank, since 1946 the median sell-off in the S&P 500 across an economic recession is 24%; some context – at the June low the S&P 500 had fallen 24.5% from its high and as of last Friday was down 18.6% from its high.

Gas prices in Europe have shot up today (Monday) following an announcement by Russia that the Nord Stream 1 pipeline to Europe would stay shut indefinitely. After three days of “maintenance”, Russia’s Gazprom decided not to turn the pipeline back on claiming the closure was due to a “technical fault”. Germany has been preparing for such a scenario and is rapidly installing temporary liquefied natural gas (LNG) terminals which will allow supplies to flow from more distant sources. European ministers will discuss special measures at an emergency meeting on Friday.

The ECB is meeting this week and there is now an increasing expectation that the central bank will lift rates by 0.75% which would be the biggest single increase in more than twenty years. Inflation in the Eurozone reached an all-time high last week rising 9.1% from a year ago. A survey of economists at the end of the week showed two-thirds think Europe has acted too slowly in battling inflation.

Markets are pricing in a 70% chance that the US Federal Reserve will also hike interest rates by 0.75% this month and the general view is that there is now less chance of rate cuts next year than previously thought. Investors have become more persuaded that the Fed will continue tightening monetary policy, whatever the data shows, until inflation is brought under control.

Goldman Sachs warned mid-week that UK inflation could top 22% next year if natural gas prices remain elevated. The Pound, relative to the US Dollar, has reached its lowest level today since March 2020. If that low is broken, which could easily happen this week, GBPUSD would be at its lowest level since 1985. This is partially due to Pound weakness but also to Dollar strength – the Dollar Index has rallied above 110 today (Monday) for the first time in nearly ten years as investors seek safety.

Also weighing on risk assets last week was the news that another major city in China had imposed a Covid-19 lockdown. According to the New York Times nearly every province has recorded infections in recent days, leaving 60 million residents locked down.

Realm Charts

UK Market Chart 2nd September 2022

US Market Chart 2nd September 2022

US Risk Barometer 2nd September 2022

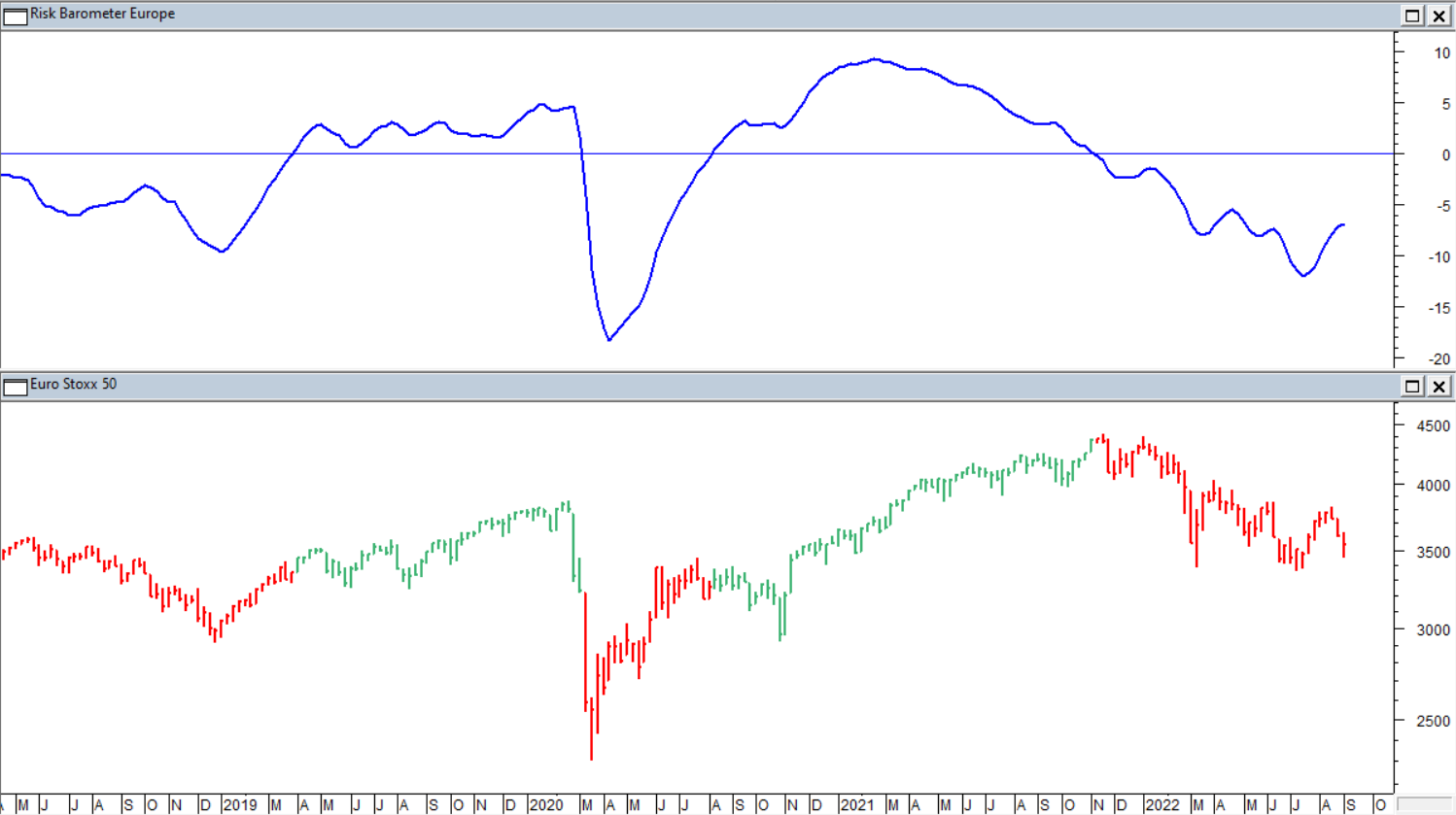

Europe Risk Barometer 2nd September 2022

{kind=link}

Disclaimer: ‘Where the business has expressed opinions, they are based on current market conditions, they may differ from those of other investment professionals and are subject to change without notice. The information contained within this communication is believed to be reliable but Realm Investment Management Limited does not warrant its completeness or accuracy.

This communication is not intended as a recommendation to invest in any particular asset class, security or strategy. Regulatory requirements that require impartiality of investment/investment strategy recommendations are therefore not applicable nor are any prohibitions to trade before publication. The information provided is for illustrative purposes only, it should not be relied upon as recommendations to buy or sell investments.’